The Generalized Dutch Disease

Evidence from the cross-section of US states

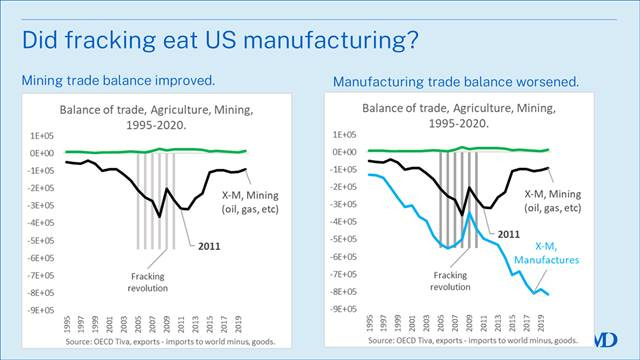

Richard Baldwin’s FactFull Friday last week suggested that the US was suffering from the Dutch Disease. He showed that the decline of US manufacturing trade balance was mirrored by the improvement in the mining trade balance.

His dispatch led me to posit a generalized Dutch disease whereby booming sectors like finance, real estate, oil, and compute coul…