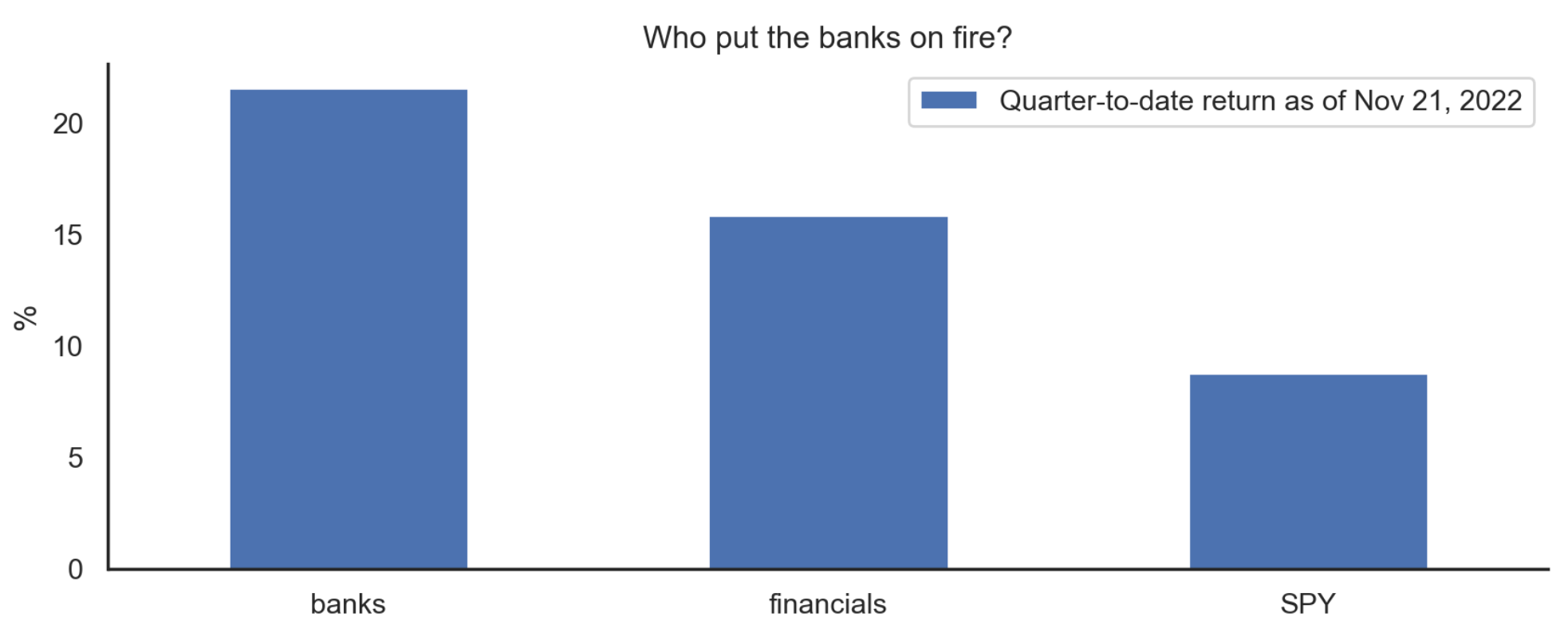

Something very strange is happening in the market for the world’s premier risk asset. While the SPY is up 8.8% quarter-to-date as of the closing auction on Monday, financials are up 15.8% and banks are up 21.6%. This is very, very strange.

To see just how strange this is, here’s the returns of the GICS sectors for reference. As I explained in the penult…

Keep reading with a 7-day free trial

Subscribe to Policy Tensor to keep reading this post and get 7 days of free access to the full post archives.