How far out are the CBO's rate assumptions?

Far out

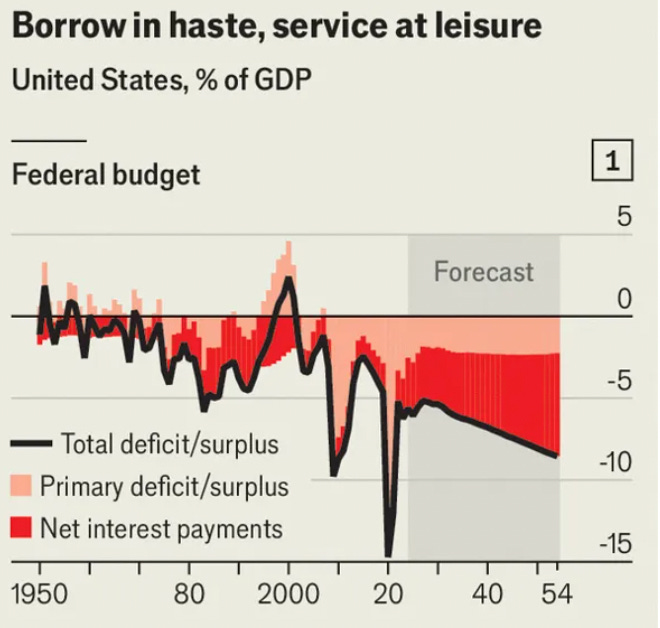

The Economist’s fiscal scold out this week features some scary looking graphs. Net interest payments, displayed in red, are projected to dominate the federal budget.

In the leader even, we find a correctly detrended but suspiciously linear forecast. What is going on here?

Keep reading with a 7-day free trial

Subscribe to Policy Tensor to keep reading this post and get 7 days of free access to the full post archives.